Last updated: June 2026

By CalcOrigin Editorial Team

What Is a Credit Card Calculator?

A credit card calculator is a specialized financial tool that helps you determine exactly how long it will take to pay off your credit card balance and how much interest you will pay along the way. Whether you are planning to make fixed monthly payments or want to pay off your balance within a specific timeframe, this credit card calculator gives you instant, accurate results so you can make informed decisions about your debt repayment strategy. Unlike a standard loan calculator, a dedicated credit card calculator accounts for the revolving nature of credit card debt and the specific way credit card interest accrues on a daily basis.

Credit card debt is one of the most expensive forms of borrowing, with average APRs hovering around 20% in 2026. Without a clear payoff plan, it is easy to fall into the trap of making only minimum payments, which can stretch your repayment timeline to decades and cost you thousands of dollars in interest. This is where a credit card calculator becomes an essential financial planning tool. By showing you the exact numbers, it helps you create a realistic repayment plan that minimizes interest costs and gets you out of debt faster. The visual payoff chart provided by the calculator makes the impact of different payment amounts immediately clear.

The credit card calculator on CalcOrigin is completely free to use and requires no personal information. Simply enter your current balance and interest rate, then choose whether you want to enter a fixed monthly payment or a target payoff date. The calculator does the rest, displaying your total interest, total payments, and a complete payoff schedule. You can even view an interactive chart that visualizes how your balance decreases over time. The payment schedule section breaks down every single payment so you can see exactly when your debt will be gone and how much each payment costs in interest versus principal reduction.

One of the most powerful features of this credit card calculator is the ability to compare different repayment scenarios side by side. You can quickly adjust your monthly payment amount and instantly see how it affects your total interest cost and payoff date. This real-time feedback helps you find the sweet spot where your monthly budget and your debt-free timeline intersect. By experimenting with different payment amounts, you can develop a strategy that balances affordability with the desire to minimize total interest costs. For managing multiple cards, try our credit card payoff calculator or explore debt consolidation options to simplify your repayment plan.

How Credit Card Interest Works

Understanding how credit card interest works is the first step toward taking control of your debt. Unlike installment loans where the interest is calculated upfront and amortized over the loan term, credit card interest is calculated based on your daily balance throughout the billing cycle. This fundamental difference means the amount of interest you pay each month depends not just on your balance and rate, but also on when you make purchases, when you make payments, and how much you carry over from the previous month. A credit card calculator handles all of this complexity automatically.

Credit card issuers use something called the average daily balance method to calculate your monthly interest. First, they determine your daily periodic rate by dividing your APR by 365. Then, they calculate the average of your daily balances over the billing cycle. The monthly interest is the product of the daily periodic rate, the average daily balance, and the number of days in the billing cycle. This is the formula our credit card calculator uses to produce accurate results that match what your credit card issuer will charge you.

One of the most important concepts to understand is the grace period. Most credit cards offer a grace period of 21 to 25 days between the statement closing date and the payment due date. If you pay your statement balance in full by the due date, you pay zero interest on new purchases. However, if you carry any balance past the due date, the grace period disappears for most cards, and interest begins accruing immediately on new purchases. This is why carrying a credit card balance is so expensive beyond just the interest rate itself. When you lose your grace period, you effectively pay interest from the day of each purchase.

Another critical concept is compound interest on credit card debt. Unlike some loans where interest is simple, credit card interest compounds daily. This means unpaid interest gets added to your principal, and future interest is calculated on the new, larger balance. The compounding effect is one reason credit card debt grows so quickly if left unchecked. A credit card calculator accounts for daily compounding to give you the most accurate possible estimate of your total interest costs over the life of the debt.

How to Calculate Credit Card Payoff

Using the credit card calculator on CalcOrigin is straightforward. The calculator is designed for two common scenarios: either you know how much you can pay each month and want to find out how long it will take, or you have a target payoff date and need to know what your monthly payment should be. Both scenarios are handled automatically by the calculator, so you do not need to perform any complex financial calculations yourself.

- Enter your credit card balance — Type in your current outstanding balance. This is the total amount you owe on the card.

- Enter your interest rate — Input your card's APR (Annual Percentage Rate). This can usually be found on your monthly statement or online account portal.

- Choose your payoff method — Select either "Pay a certain amount" to enter a fixed monthly payment, or "Pay off within a certain timeframe" to set a target payoff date.

- Click Calculate — The credit card calculator instantly displays your payoff time, total interest, total amount paid, and a complete schedule.

The quick select feature lets you choose common payment amounts based on a percentage of your balance plus interest. For example, "Interest + 1%" means your monthly payment equals the interest charges plus 1% of the principal balance. This is how many credit card issuers calculate minimum payments, and using this feature helps you see exactly how long the minimum payment path would take. Trying different quick select options gives you immediate insight into how different payment strategies affect your total interest costs and payoff timeline.

Understanding Credit Card APR

APR stands for Annual Percentage Rate, and it represents the total yearly cost of borrowing on your credit card. However, despite the name, credit card interest is not calculated annually. Instead, it is calculated daily based on your outstanding balance, which is why your credit card calculator needs to convert the APR to a daily periodic rate to produce accurate results.

Most credit cards have a variable APR that fluctuates with the prime rate. The prime rate is the benchmark interest rate that banks charge their best customers, and it changes based on the federal funds rate set by the Federal Reserve. When the Fed raises rates, your credit card APR typically increases as well. This means your repayment plan may need periodic adjustments if rates change significantly.

Credit cards can have multiple APRs for different types of transactions. There is usually a purchase APR for regular purchases, a cash advance APR for cash withdrawals (which tends to be higher), and a balance transfer APR for transferred balances. Some cards also offer promotional 0% APR periods for new purchases or balance transfers. Understanding which APR applies to your balance is important for accurate calculations with your credit card calculator.

Average Daily Balance Method

The average daily balance method is the standard way credit card issuers calculate interest charges. While the formula may seem complex at first, understanding it helps you see why making payments early in your billing cycle can save you money. The credit card calculator on CalcOrigin uses this exact method to give you realistic results that match what your credit card company would charge.

Daily Periodic Rate (DPR) = APR / 365

Monthly Interest = DPR × Average Daily Balance × Days in Billing Cycle

Here is a concrete example. Suppose you have a $5,000 balance on a card with an 18% APR. Your daily periodic rate is 0.0493% (18% divided by 365). If your average daily balance over a 30-day billing cycle is $5,000, your monthly interest would be 0.000493 × $5,000 × 30 = $73.95. Now imagine you make a $1,000 payment on day 15 of the billing cycle. Your average daily balance drops to about $4,500, and your interest drops to $66.56. That $1,000 payment saves you about $7.39 in interest for that single month.

This example illustrates a key insight: making payments earlier in your billing cycle reduces your average daily balance more than making the same payment later. Some financial experts recommend making bi-weekly payments rather than monthly payments specifically because it lowers the average daily balance and saves on interest. Your credit card calculator assumes a standard monthly payment schedule, making it a conservative estimate of your potential savings. If you make payments more frequently than once per month, your actual savings could be even greater than what the calculator shows.

It is also worth understanding that credit card companies use different methods for calculating the average daily balance. The most common approach includes new purchases in the balance from the day they post to your account. However, some issuers offer a grace period on new purchases even when you carry a balance, though this is increasingly rare. The credit card calculator on CalcOrigin uses the most common method, which assumes new purchases begin accruing interest immediately when you carry a balance from the previous month.

Minimum Payment Impact

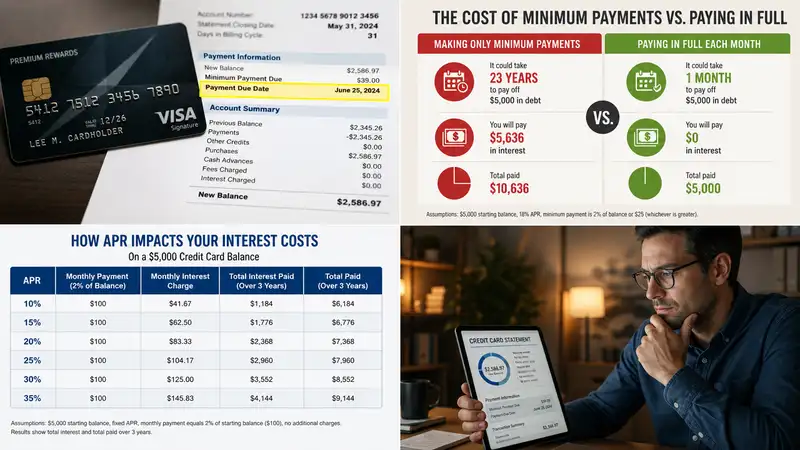

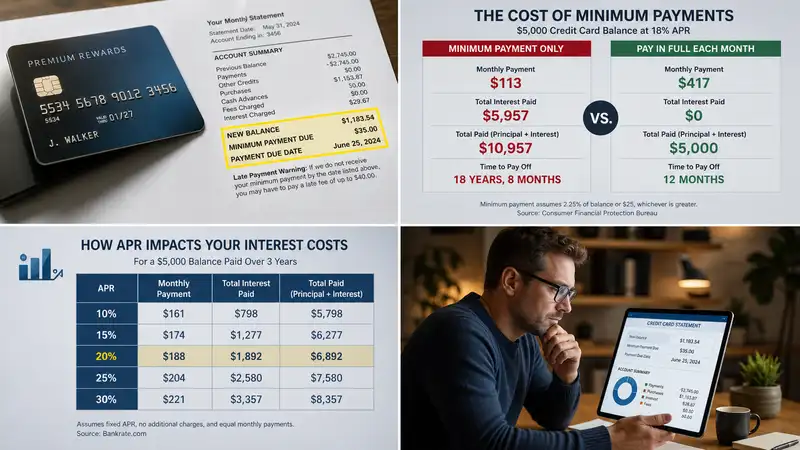

One of the most eye-opening features of the credit card calculator is seeing the real cost of making only minimum payments. Most credit card issuers calculate your minimum payment as 1% to 3% of your outstanding balance, or a flat amount like $25 to $35, whichever is greater. While this keeps your monthly payment low, it also means most of your payment goes toward interest rather than principal, and the debt shrinks very slowly. Understanding why minimum payments are so costly is crucial for developing an effective payoff strategy.

Consider a real-world example. With a $5,000 balance at 18% APR and a minimum payment of 2% of the balance (or $25, whichever is greater), the credit card calculator shows that it would take over 20 years to pay off the debt, and you would pay more than $7,000 in total interest. That is more than double the original balance just in interest charges. Many people are shocked when they first see these numbers, which is why using a credit card calculator before committing to a payment plan is so important. The calculator makes the long-term cost of minimum payments concrete and impossible to ignore.

The impact of paying just a little more than the minimum is dramatic. Using the same $5,000 balance at 18% APR, increasing your monthly payment from 2% to 3% of the balance cuts the repayment time by more than half and saves thousands of dollars in interest. This is the power of the credit card calculator — it shows you exactly how much difference a slightly larger payment can make over the life of the debt. Even an extra $20 or $30 per month can shave years off your repayment timeline and save hundreds or thousands of dollars in interest.

The credit card calculator also reveals an important insight about the early stages of repayment. In the first months of minimum payments, nearly all of your payment goes toward interest. For a $5,000 balance at 18% APR, the first month's interest is about $75, and if your minimum payment is $100, only $25 actually reduces your principal. The credit card calculator shows this breakdown clearly in the payment schedule, helping you understand why getting ahead of the minimum payment curve is so critical in the early months of repayment.

Debt Avalanche vs. Snowball Method

When you have credit card debt, two popular strategies can help you decide which card to pay off first: the debt avalanche method and the debt snowball method. A credit card calculator can help you analyze both approaches so you can choose the one that works best for your situation.

The debt avalanche method focuses on paying off the card with the highest interest rate first while making minimum payments on all other cards. This approach minimizes the total interest you pay over time, making it the mathematically optimal strategy. Using a credit card calculator for each of your cards, you can determine exactly how much interest each card is costing you and prioritize accordingly.

The debt snowball method focuses on paying off the smallest balance first regardless of interest rate, while making minimum payments on larger balances. This approach prioritizes psychological wins over mathematical efficiency. As each small balance is eliminated, the motivation gained from these quick wins can help you stay committed to your debt payoff plan. The credit card calculator helps you set realistic payment amounts for each card under either strategy.

Balance Transfer Strategy

A balance transfer involves moving your existing credit card debt to a new card, typically one offering a 0% introductory APR for 12 to 18 months. This can be an effective way to accelerate your debt repayment since every dollar of your payment goes toward the principal rather than interest during the promotional period. A credit card calculator is invaluable for planning a balance transfer strategy because it shows you exactly how much you need to pay each month to eliminate the balance before the promotional period ends.

Most balance transfers charge a fee of 3% to 5% of the transferred amount. This means transferring a $5,000 balance would cost $150 to $250 upfront. To determine whether a balance transfer is worth it, use a credit card calculator to compare the total interest you would pay on your current card versus the transfer fee plus any interest you might pay if you do not fully repay during the promotional period. In many cases, the savings from avoiding even a few months of high-interest charges outweighs the transfer fee, making the balance transfer a net positive move.

However, balance transfers require discipline. Once the promotional APR period expires, the remaining balance is subject to the standard APR, which is often higher than your original card. The credit card calculator can help you create a payment schedule that ensures you pay off the full balance before the promotional period ends. It also helps you understand what happens if you fall short — showing you the interest costs if any balance remains when the standard APR kicks in. This is particularly valuable for planning contingency scenarios.

When evaluating balance transfer offers, pay attention to three key factors beyond the promotional APR. First, the transfer fee percentage and whether there is a cap on the fee amount. Second, the length of the promotional period and whether it applies to new purchases as well as transferred balances. Third, the standard APR that will apply after the promotional period ends. Each of these factors affects your total cost, and a credit card calculator can help you model different scenarios to find the best balance transfer offer for your specific situation.

Advantages and Disadvantages of Credit Cards

Understanding the advantages and disadvantages of credit cards helps you use them responsibly and avoid common pitfalls. A credit card calculator is an essential tool for managing the financial aspects, but the behavioral aspects of credit card use matter just as much.

Advantages of Credit Cards:

- Safety and Convenience — Carrying a credit card is safer than carrying cash. If your card is lost or stolen, you are protected by zero-liability fraud protection.

- Build Credit History — Responsible credit card use, including on-time payments and low credit utilization, helps build a strong credit profile that can improve your access to mortgages and auto loans.

- Rewards and Benefits — Many cards offer cashback (1% to 2% on purchases), travel points, purchase protection, extended warranties, and travel insurance. Using a credit card calculator to track your spending helps you maximize these benefits without carrying a balance.

- Emergency Buffer — A credit card can provide short-term liquidity during unexpected expenses, though a credit card calculator should be used to plan repayment as quickly as possible.

Disadvantages of Credit Cards:

- High Interest Rates — With average APRs around 20%, carrying a balance is one of the most expensive forms of borrowing. A credit card calculator shows you exactly how much this costs.

- Debt Accumulation Risk — The ease of swiping a card can lead to spending beyond your means. Without a budget and a credit card calculator to track repayment, debt can quickly spiral out of control.

- Fees — Annual fees, late payment fees, over-limit fees, and cash advance fees can add hundreds of dollars to your annual costs. Factor these into your credit card calculator analysis for a complete picture.

- Credit Score Impact — High credit utilization (using more than 30% of your available credit) can lower your credit score, even if you make payments on time.

Credit Card Tips for Smart Usage

Using credit cards wisely is about more than just picking the right card. It is about developing habits that keep you in control of your finances. A credit card calculator supports these habits by giving you clear, numeric feedback on your decisions. Here are practical tips for smart credit card use that can help you avoid common pitfalls and make your cards work for you rather than against you.

Pay your statement balance in full each month. This is the single most important rule of credit card use. When you pay in full by the due date, you never pay a penny of interest and you maintain your grace period for the next month. Your credit card calculator can help you understand what happens when you break this rule by showing you the true cost of carrying a balance, but the goal should always be to avoid carrying a balance in the first place.

Keep your credit utilization below 30%. Your credit utilization ratio is the amount you owe divided by your total credit limit. A ratio above 30% can lower your credit score, even if you pay in full each month. If you consistently use more than 30% of your available credit, request a credit limit increase or consider an additional card to spread out your balance. The credit card calculator can help you plan how quickly to pay down a high balance to bring your utilization back into a healthy range.

Set up automatic payments. Late payments can trigger penalty APRs of 29% or higher and damage your credit score by as much as 100 points. Setting up autopay for at least the minimum payment ensures you never miss a due date. Use a credit card calculator to plan your payment amount and schedule those automatic transfers accordingly. Even one late payment can cost you hundreds of dollars in penalty interest over the following months.

Avoid cash advances. Cash advances on credit cards have higher interest rates than regular purchases, and interest begins accruing immediately with no grace period. Most cards also charge a cash advance fee of 3% to 5% with a minimum fee of $10. If you need cash, a personal loan or line of credit from your bank is almost always a cheaper option. The credit card calculator can show you just how expensive cash advances are compared to regular purchases.

Review your statements monthly. Check each month's statement for unauthorized charges, billing errors, and changes to your APR or terms. The earlier you catch a problem, the easier it is to resolve. Your credit card calculator can help you verify that the interest charges on your statement match what you expect based on your average daily balance and APR, helping you catch billing errors that might otherwise go unnoticed.

Take advantage of rewards without overspending. Cashback and travel rewards are valuable benefits, but they only help you if you pay your balance in full each month. Carrying a balance at 20% APR while earning 2% cashback means you are losing 18% net on every dollar. Use a credit card calculator to see this math for yourself and understand why rewards cards only make financial sense for people who never carry a balance.

Avoid closing old credit card accounts. Closing a credit card reduces your total available credit, which increases your credit utilization ratio and can lower your credit score. It also shortens your average account age, another factor in credit scoring. Instead of closing an old card, keep it open with a small recurring charge that you pay off monthly. A credit card calculator helps you focus on paying down balances rather than closing accounts.

To learn more about credit card calculator, visit Fannie Mae.

Frequently Asked Questions

How is credit card interest calculated?

Credit card interest is typically calculated using the average daily balance method. The issuer calculates your daily periodic rate by dividing your APR by 365, then multiplies this by your average daily balance and the number of days in the billing cycle.

What is APR on a credit card?

APR stands for Annual Percentage Rate. It represents the yearly interest rate charged on unpaid credit card balances. Most credit cards have variable APRs based on the prime rate plus a margin.

What is the minimum payment on a credit card?

Minimum payments are typically 1-3% of your balance or a fixed amount (usually $25-$35), whichever is greater. Paying only the minimum means you will pay much more in interest over time.

How can I pay off my credit card faster?

Pay more than the minimum each month, focus on high-interest cards first (debt avalanche), consider balance transfers to lower-rate cards, and avoid new charges while paying off existing debt.

Should I pay off my credit card in full every month?

Yes, if possible. Paying your full balance by the due date avoids all interest charges. This is the most responsible way to use credit cards and maximizes any rewards or benefits you receive.

What is the average daily balance method?

The average daily balance method sums your balance each day of the billing cycle and divides by the number of days. Your daily periodic rate (APR divided by 365) is then multiplied by this average and by the days in the cycle to determine interest charges for the month.

What is a good credit card APR?

A good credit card APR is typically between 8% and 12%, though the national average hovers around 20%. The lowest rates are usually reserved for borrowers with excellent credit scores above 740. Introductory 0% APR offers can last 12-18 months but revert to the standard APR afterward.

Does checking my credit card balance affect my credit score?

Checking your own credit card balance does not affect your credit score. This is considered a soft inquiry. However, your credit utilization ratio (how much of your available credit you are using) does affect your score. Keeping your utilization below 30% is generally recommended.

What happens if I only make the minimum payment?

If you only make the minimum payment each month, it can take years or even decades to pay off your balance, and you will pay significantly more in interest. For example, a $5,000 balance at 18% APR with a $100 minimum payment takes over 7 years to repay and costs more than $3,500 in interest.

What is a balance transfer on a credit card?

A balance transfer moves your existing credit card debt to a new card, often with a 0% introductory APR for 12-18 months. This allows you to pay down the principal without accruing interest during the promotional period. Balance transfers typically carry a fee of 3% to 5% of the transferred amount.

How does a credit card grace period work?

A grace period is the time between your statement closing date and your payment due date, typically 21-25 days. If you pay your statement balance in full by the due date, no interest is charged on new purchases. Grace periods do not apply to cash advances or balance transfers.

Can this calculator help me with multiple credit cards?

This calculator is designed for single credit card analysis. If you have multiple credit cards, try our credit card payoff calculator which allows you to enter multiple balances and interest rates to find the optimal payoff strategy using either the debt avalanche or debt snowball method.