Last updated: June 2026

By CalcOrigin Editorial Team

What is a Debt-to-Income Ratio?

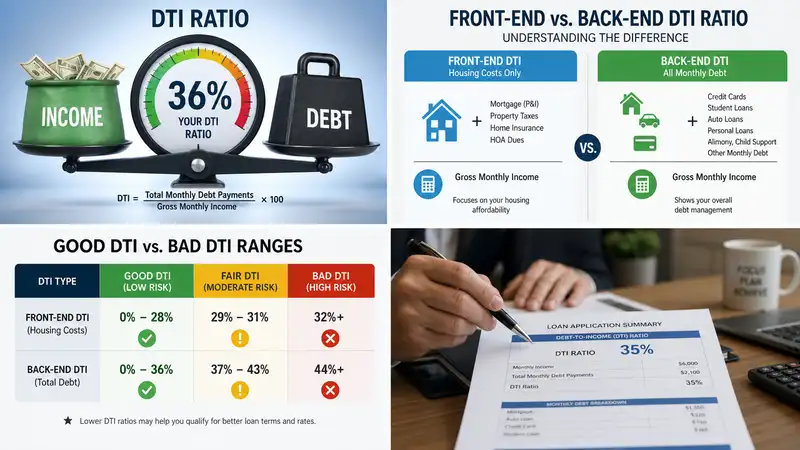

Debt-to-income ratio (DTI) is the ratio of total debt payments divided by gross income (before tax) expressed as a percentage, usually on either a monthly or annual basis. It is one of the most critical metrics lenders use to determine whether you can afford to take on additional debt, particularly for mortgages, auto loans, and personal loans.

A lower DTI indicates a healthy balance between debt and income, suggesting that you have sufficient income to manage your monthly obligations comfortably. Conversely, a high DTI signals that a significant portion of your income goes toward debt payments, leaving less room for additional financial commitments or unexpected expenses.

There is a separate ratio called the credit utilization ratio (sometimes called debt-to-credit ratio) that works slightly differently. The debt-to-credit ratio is the percentage of how much a borrower owes compared to their credit limit and has an impact on their credit score. While DTI focuses on income versus debt payments, credit utilization focuses on how much of your available credit you are actually using. Understanding both ratios gives you a complete picture of your financial health and helps you target the right areas for improvement.

Front-End Ratio

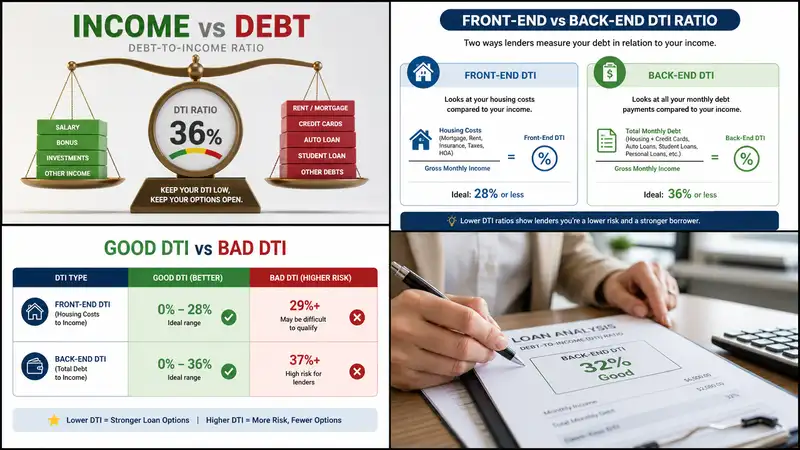

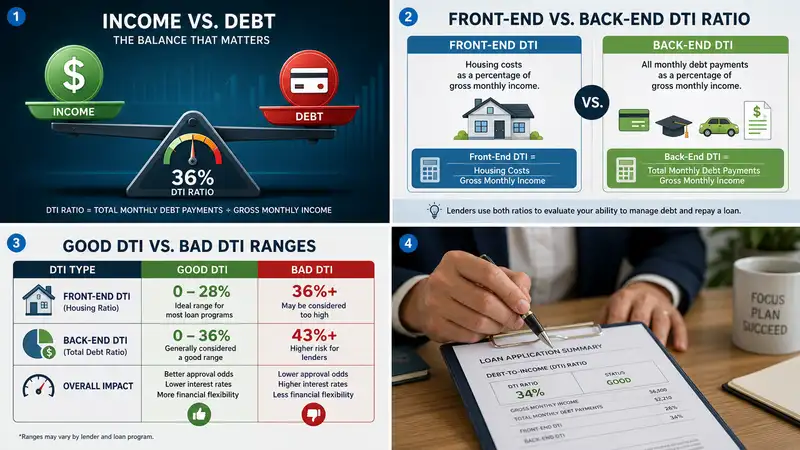

Front-end debt ratio, sometimes called mortgage-to-income ratio in the context of home-buying, is computed by dividing total monthly housing costs by monthly gross income. The front-end ratio includes not only rental or mortgage payment, but also other costs associated with housing like insurance, property taxes, HOA/Co-Op Fee, etc. This ratio specifically focuses on housing expenses because they typically represent the largest single category of monthly debt for most households.

For renters, the front-end ratio helps landlords assess whether you can afford the rent. For homeowners, it helps mortgage lenders determine the maximum loan amount they are willing to offer. A low front-end ratio indicates that your housing costs are well within your means, while a high ratio may suggest you are housing-cost burdened.

In the U.S., the standard maximum front-end limit used by conventional home mortgage lenders is 28%. However, this threshold can vary by lender, loan program, and geographic area. In high-cost housing markets, some lenders may accept higher front-end ratios with compensating factors such as excellent credit or substantial cash reserves.

Back-End Ratio

Back-end debt ratio is the more all-encompassing debt associated with an individual or household. It includes everything in the front-end ratio dealing with housing costs, along with any accrued monthly debt like car loans, student loans, credit cards, personal loans, and other recurring financial obligations such as child support or alimony payments.

Lenders place significant weight on the back-end ratio because it provides a complete picture of your monthly financial obligations. Even if your front-end ratio is low, a high back-end ratio due to substantial non-housing debt may still disqualify you from certain loans. This is why it is important to manage all forms of debt, not just housing costs.

In the U.S., the standard maximum limit for the back-end ratio is 36% on conventional home mortgage loans. Some government-backed loans and portfolio loans may accept higher ratios, but borrowers with back-end ratios above 43% often face difficulty qualifying for prime lending rates.

House Affordability

In the United States, lenders use DTI to qualify home-buyers. Normally, the front-end DTI/back-end DTI limits for conventional financing are 28/36, the Federal Housing Administration (FHA) limits are 31/43, and the VA loan limits are 41/41. These thresholds are not arbitrary; they are based on decades of lending data showing which ratios correlate with on-time mortgage payments and lower default rates.

When you apply for a mortgage, lenders calculate both your front-end and back-end DTI ratios using documented income and verified debt obligations. If your ratios exceed the program limits, you may need to reduce debt, increase your down payment, or consider a different loan program with higher allowable ratios.

While DTI ratios are widely used as technical tools by lenders, they can also be used to evaluate personal financial health. Normally, a DTI of 1/3 (33%) or less is considered to be manageable. A DTI of 1/2 (50%) or more is generally considered too high, indicating that more than half of your gross income goes toward debt payments each month. Keeping your DTI within these ranges not only improves your loan eligibility but also provides greater financial flexibility for unexpected expenses and future goals.

How to Calculate Your Debt-to-Income Ratio

Calculating your debt-to-income ratio is straightforward. The formula is: DTI = (Total Monthly Debt Payments / Gross Monthly Income) x 100. The result is a percentage that represents what portion of your income goes toward debt obligations each month.

For example, if your gross monthly income is $5,000 and your total monthly debt payments are $1,650, your DTI ratio would be 33%. To calculate, divide $1,650 by $5,000 to get 0.33, then multiply by 100 to get 33%. This means 33% of your gross monthly income goes toward debt payments, which is generally considered a healthy ratio.

Here is another example: Suppose you earn $4,200 per month before taxes. Your monthly debts include a $1,200 rent payment, a $350 car loan, $150 in minimum credit card payments, and $100 in student loans, totaling $1,800. Your DTI would be $1,800 divided by $4,200, or approximately 43%. This is near the upper limit for most conventional loans.

Your monthly debt payments include items like rent or mortgage, car loans, student loans, credit card minimum payments, personal loans, and any other recurring obligations. Your gross monthly income is your income before taxes and deductions, including salary, wages, bonuses, tips, investment income, and any other regular earnings from sources like alimony or child support.

Use our DTI calculator above to quickly compute your ratio without manual math. Simply enter your income sources and debt obligations, and the calculator handles the rest, including converting between monthly and annual figures automatically.

One important nuance in DTI calculation is how lenders treat different types of income and debt. For example, part-time income may only be counted if you have a two-year history of consistent earnings. Rental income from investment properties is typically counted at 75% of gross rent (the standard 25% vacancy factor). Child support and alimony may be counted as income if you can document consistent receipt. Understanding these nuances helps you present the strongest possible financial picture when applying for a loan.

On the debt side, lenders typically count the minimum payment shown on your credit report for revolving accounts like credit cards, even if you pay the full balance each month. For installment loans, they use the actual monthly payment. Student loans in deferment or forbearance may still be counted at 1% of the outstanding balance or the standard monthly payment, whichever is higher. These lender-specific calculations mean your DTI for a mortgage application may differ slightly from the general calculation you do at home.

Why Lenders Care About Your DTI Ratio

Lenders use your debt-to-income ratio as a key risk assessment tool. A high DTI signals that you may struggle to make additional loan payments, increasing the likelihood of default. This is why mortgage lenders, auto lenders, and personal loan providers all evaluate your DTI before approving applications. It is one of several factors considered alongside your credit score, employment history, and down payment size.

Each lender has its own DTI thresholds. Conventional mortgage lenders typically cap the back-end DTI at 36%, while FHA loans allow up to 43%. Some portfolio loans may accept DTIs as high as 50% with compensating factors like a large down payment or excellent credit history. Auto lenders tend to be more flexible, often approving borrowers with DTIs up to 45-50% depending on credit scores.

Your DTI ratio also affects the interest rate you are offered. Borrowers with lower DTIs generally qualify for lower rates because they present less risk to lenders. Even a small difference in interest rates can translate into significant savings over the life of a loan. For example, reducing your mortgage rate by just 0.5% on a $300,000 loan could save you over $25,000 in interest over 30 years.

Understanding how DTI affects lending decisions can help you prepare before applying for credit. Check your credit score alongside your DTI for a complete picture of your financial health.

Beyond initial approval, your DTI can influence other loan terms including the required down payment, mortgage insurance requirements, and documentation level needed. Borrowers with lower DTIs may qualify for streamlined documentation programs that require less paperwork and faster processing times. Some lenders also offer pricing adjustments based on DTI, meaning a lower ratio could save you money on origination fees and discount points.

It is also worth noting that DTI requirements can shift with economic conditions. During periods of economic uncertainty, lenders may tighten their DTI limits to reduce risk. Conversely, in a competitive lending environment, some lenders may offer more flexible DTI thresholds to attract borrowers. Staying informed about current lending standards in your market helps you time your loan application for the best possible terms.

6 Tips to Improve Your Debt-to-Income Ratio

Improving your debt-to-income ratio takes time and discipline, but the payoff is worth it. A lower DTI can help you qualify for better loan terms, lower interest rates, and larger loan amounts. Lenders view a low DTI as a sign of financial stability, which can open doors to more favorable financing options across all types of credit. Here are six proven strategies to improve your DTI:

- Pay down high-interest debt first. Focus on credit cards and personal loans with the highest interest rates, as these typically have the largest monthly minimum payments relative to their balance. Use a debt payoff calculator to create a repayment strategy that works for your budget. The debt avalanche method prioritizes highest-interest debt first, saving you the most money over time.

- Avoid taking on new debt. Delay major purchases like cars, furniture, or appliances until after you secure a mortgage or other important financing. Every new monthly payment increases your DTI and reduces your borrowing power. Even financing a new phone or appliance through store credit can add $50-100 to your monthly obligations, which could push your DTI over a lender's threshold.

- Increase your income. Consider a side hustle, freelance work, overtime hours, or asking for a raise. Additional income reduces your DTI even if your debt stays the same, and it can make a meaningful difference when you are close to a lender's DTI threshold. Even an extra $500 per month can lower your DTI by several percentage points.

- Consider debt consolidation. Combining multiple debts into a single lower-interest loan can reduce your monthly payments and simplify your finances. Use a loan calculator to compare consolidation options and see how much you could save each month. Balance transfer credit cards and personal loans are common consolidation tools that can lower your interest rate and monthly payment simultaneously.

- Pay more than the minimum. Making extra payments on loans reduces principal faster and lowers your overall debt burden over time. Even an additional $50 per month toward your highest-interest debt can accelerate your progress significantly. Consider applying windfalls like tax refunds, bonuses, or gifts directly to your debt balances.

- Use a longer loan term strategically. Refinancing a loan to extend its term lowers the monthly payment, which improves your DTI in the short term. This can be useful when preparing for a mortgage application, but be aware that longer terms typically increase total interest paid over the life of the loan.

Remember that improving your DTI is a gradual process. Focus on consistent progress rather than overnight results, and monitor your ratio monthly using this calculator to track your improvement. Even small improvements can make a meaningful difference in your borrowing power.

Common Mistakes to Avoid When Calculating DTI

Avoid these common mistakes to ensure your DTI calculation accurately reflects your financial situation:

Using net income instead of gross income. DTI is always calculated using gross (pre-tax) income. Using take-home pay will overstate your ratio and give an inaccurate picture. Always use your income before taxes, retirement contributions, and other deductions.

Forgetting periodic expenses. Annual expenses like property taxes or insurance premiums should be divided by 12 to get accurate monthly figures. Our calculator handles this automatically by letting you choose monthly or yearly periods for each expense.

Excluding all debt obligations. Some borrowers forget to include alimony, child support, personal loans, or other recurring payments. Include every recurring debt to get an accurate DTI. When in doubt, include the expense and let the numbers tell the story.

Confusing DTI with credit utilization. DTI measures debt against income, while credit utilization measures credit card balances against credit limits. Both matter for different reasons, and understanding the distinction helps you manage both effectively.

Using outdated income or debt figures. Your DTI changes as your income and debts change. Always use your most current numbers for the most accurate assessment, especially before applying for a major loan.

Ignoring irregular income. If you work on commission, receive bonuses, or have variable income, use a conservative average rather than your best month. Lenders typically average your income over the most recent two years, so understanding how your variable income is treated can help you avoid surprises during the loan application process.

Not checking all three credit reports. Errors on your credit report can include debts that are not yours or incorrectly reported balances, both of which can inflate your DTI. Review your credit reports annually from all three major bureaus and dispute any inaccuracies before applying for a major loan. Even small errors can push your DTI above a lender's threshold.

Avoiding these mistakes ensures that your DTI calculation accurately reflects your financial situation and gives you the clearest picture of your borrowing power. When in doubt, the conservative approach is always better.

DTI Ratio vs. Credit Utilization Ratio

While both ratios measure financial health, they serve different purposes. Your debt-to-income ratio compares your total monthly debt payments to your gross monthly income and is used primarily by lenders to evaluate loan eligibility. It answers the question: can you afford to take on more debt given your current income?

Your credit utilization ratio compares your credit card balances to your credit limits and directly impacts your credit score. A low credit utilization ratio (under 30%) is generally recommended for good credit health. This ratio answers a different question: how much of your available revolving credit are you using?

Both ratios are important, but they affect different aspects of your financial life. DTI determines how much you can borrow and whether you qualify for loans, while credit utilization influences your borrowing costs through your credit score. Lenders evaluate both ratios, along with your payment history and employment stability, to make comprehensive lending decisions.

A key distinction is that DTI includes all types of debt (mortgages, car loans, student loans, etc.), while credit utilization only applies to revolving credit accounts like credit cards and lines of credit. Managing both ratios effectively is essential for optimal financial health.

Here is a practical example of how the two ratios differ: Imagine you earn $6,000 per month and have a $1,500 mortgage payment and a $300 car loan. Your DTI is 30% ($1,800 divided by $6,000). Now suppose you have a credit card with a $10,000 limit and a $2,000 balance. Your credit utilization ratio is 20% ($2,000 divided by $10,000). The DTI tells lenders whether you can afford additional monthly payments, while the credit utilization ratio influences your credit score and therefore the interest rate you will be offered.

Both ratios should be monitored regularly, but the strategies for improving each differ. To lower DTI, focus on increasing income and paying down installment debt. To lower credit utilization, focus on paying down credit card balances and avoiding maxing out your revolving accounts. A balanced approach that addresses both ratios gives you the strongest financial profile for any lending situation.

DTI Ratio Requirements by Loan Type

Different loan types have varying DTI requirements, and understanding these differences can help you choose the right loan program for your situation:

Conventional loans typically follow the 28/36 rule, capping front-end DTI at 28% and back-end DTI at 36%. These loans often require private mortgage insurance (PMI) if the down payment is less than 20%. Conventional loans are the most common mortgage type and generally offer the most competitive rates for borrowers with strong credit and low DTI.

FHA loans, insured by the Federal Housing Administration, are more flexible with maximum DTI ratios of 31% front-end and 43% back-end. FHA loans are popular with first-time homebuyers due to their lower down payment requirements, which can be as low as 3.5% of the purchase price. However, FHA loans require both an upfront and annual mortgage insurance premium.

VA loans, available to veterans and active military, have no specific DTI limit but generally expect a 41% back-end ratio or lower. VA loans offer competitive rates and do not require a down payment or PMI, making them one of the most affordable mortgage options for eligible borrowers.

USDA loans, designed for rural homebuyers, typically require a back-end DTI of 41% or less. These loans offer 100% financing with no down payment requirement for eligible properties in designated rural areas. USDA loans also feature lower mortgage insurance costs compared to FHA loans.

Use our mortgage calculator to estimate payments based on different loan scenarios and see how your DTI affects affordability. Understanding your DTI before applying can save time and help you target loan programs where you are most likely to qualify.

Debt-to-Income Ratio for Business and Self-Employed

Self-employed individuals and business owners face unique challenges when calculating DTI for loan applications. Unlike salaried employees who can provide recent pay stubs as income verification, self-employed borrowers must typically provide two years of tax returns to verify income. Lenders use the average of the most recent two years of net income rather than current cash flow, which can sometimes result in a lower qualifying income than expected.

For business owners, it is important to distinguish between business debt and personal debt. Business loans and expenses that appear on personal credit reports will count toward your personal DTI. Separating business and personal finances with dedicated bank accounts and credit cards can help present a clearer picture to lenders and keep business debts from inflating your personal DTI unnecessarily.

If you are self-employed, consider working with a loan officer experienced in self-employed borrowing. They can help you understand which income documentation the lender will use and how business debts are treated in the DTI calculation. Some lenders offer bank statement loan programs that use recent deposits instead of tax returns, which can be beneficial for self-employed borrowers who take significant business deductions.

Planning ahead is essential. If you anticipate applying for a mortgage in the next year or two, consider how your business structure and tax strategies affect your reported income and DTI. A conversation with both your accountant and a mortgage professional can help you prepare.

Self-employed borrowers should also be aware that lender requirements for documentation have evolved in recent years. Many lenders now offer alternative documentation programs that use bank statements or business profit-and-loss statements in addition to tax returns. These options can be particularly helpful for self-employed borrowers whose tax returns show significant deductions that reduce adjusted gross income. Exploring multiple lenders to find one familiar with self-employed income structures is well worth the effort.

Final Thoughts on Debt-to-Income Ratios

Your debt-to-income ratio is one of the most important metrics for understanding your financial health and borrowing power. Whether you are planning to buy a home, refinance existing debt, or simply want to improve your financial standing, monitoring your DTI regularly is essential. A healthy DTI not only opens doors to better loan options but also provides peace of mind that your debt levels are manageable.

The key to a good DTI is balance. While some debt is normal and even beneficial for building credit, too much debt relative to your income can limit your financial flexibility and opportunities. By keeping your DTI within recommended ranges, you position yourself for financial success whether you are buying a home, financing a car, or pursuing other financial goals.

Use our Debt-to-Income Ratio Calculator above to compute your current DTI, then explore our budget calculator and house affordability calculator to plan your next financial move. With a healthy DTI, you will be better positioned to qualify for loans, secure favorable interest rates, and achieve your financial goals.

Remember that your DTI is not a static number. As your career progresses and your income grows, your ratio naturally improves even without paying down debt. Similarly, major life events like marriage, which combines two incomes, can significantly improve your household DTI. The key is to remain mindful of how new debt commitments affect your ratio and to plan major purchases strategically around your long-term financial objectives.

Whether you are a first-time homebuyer, a seasoned investor, or someone simply looking to improve their financial health, understanding and monitoring your debt-to-income ratio is a fundamental skill that pays dividends throughout your financial life. Start by calculating your current DTI today, set targets for improvement, and revisit your progress regularly to stay on track toward your financial goals.

To learn more about debt ratio calculator, visit Consumer Financial Protection Bureau.